Think You Can’t Afford An Investment Property?

Your Property Experts were proud to present recently at an Educational Seminar on the topic of investing in property exclusively for the members of Inner West Mums. Since then they’ve been inundated with requests for copies of the presentation from those who weren’t able to attend on the event but who are really interested to learn more about investing in property.

So they’ve put together a series of articles highlighting some of the key topics discussed on the night.

In this first article, finance expert Louisa Sanghera from Zippy Finance explains just how you can finance the purchase of an investment property…even if you THINK you can’t afford to …

We speak to potential investors on a daily basis who are keen to build their personal wealth by investing in property. They tend to fall into 2 categories:

- Currently renting and can’t afford to buy where they live – Those currently renting typically are looking to become rentvestors. Rentvesting is a fairly new term coined to describe those investors who continue to rent the home they live in and purchase a property to invest elsewhere. This particular strategy is very popular for those living in expensive areas such as Sydney’s Inner West who want to get onto the property ladder but simple can’t afford the price of property in that area.

- Home owners with equity in their owner occupied property – Many home owners believe that because they already have what potentially could be a very large mortgage, that they can’t afford to purchase an investment property. For some, that may indeed be true, but for those with substantial equity in their home, they may still be able to use that equity to fund the purchase of an investment.

In this article, I’ll be exploring some of the ways these two groups of potential investors CAN grow their wealth by investing in property. But first, let’s look at a couple of the key terms in finance which you’ll need to understand ……

Lender’s Mortgage Insurance (LMI)

LMI is payable when borrowing more than 80% of a property’s value. It is designed to provide lenders with an extra level of protection in case the borrower defaults on their loan. While expensive, it has allowed a great many to purchase a home even with a very small deposit.

LMI can be very expensive, but you should weigh this up against the potential gains from the particular property you are seeking to purchase. The potential long term capital gain may well out weight the costs of the LMI.

Loan To Value Ratio (LVR)

The LVR is the amount you are borrowing, represented as a percentage of the value of the property being used as security for the loan. Lenders place a large emphasis on this when they are assessing your loan application and the lower the LVR , the lower the risk is to the bank.

Investment Loan Deposit

So exactly how much of a deposit DO you need?

The answer is simple …the same as you would need for a home loan deposit with a maximum loan to value ratio of 95%.

While having saved for a deposit is the ideal situation, borrowers don’t actually need to have the deposit sitting readily available as cash savings. You can withdraw the deposit from your equity on your owner-occupied property or you can even be gifted the amount due. It is however important to bear in mind that the amount of deposit you have will affect the interest rate you are offered.

Choosing A Loan That’s Right For You

Lenders have tightened up on borrowers for investment purposes but there are still many options available and it’s important to understand the different options available :

- Variable Rate – With a variable interest rate, your rate will move up and down in line with mortgage interest rates. Your monthly repayments can vary widely during the term of your loan and it is important to always allow for future rate rises, especially in the current climate where rates have already begun to rise.

- Fixed Rate – A fixed rate loan locks you in to a particular interest rate for a specific period so your repayment will remain the same. Fixed rate loans are popular for borrowers who need to know in advance what their payments will be for a specific period of time. There are typically additional upfront fees called “rate lock” fees with a fixed rate home loan though and they don’t all come with an offset facility.

- Split Loans – These divide your loan into fixed and variable rate portions.

- Line of Credit – This combines your home loan with an everyday transaction account from which the borrower can draw cash up to a pre-approved limit.

- Low Doc Loans – These are useful for borrowers who are unable to provide conventional income documentation or for people with complex structures.

Home Buying Costs

When buying a property, there are several upfront costs. Some of which you’ll expect but especially for first time buyers, there are some costs you might not be aware of. So what exactly are the costs of purchasing a home …..

- Deposit for property (minimum 5%)

- Pre-purchase inspections e.g. pest and building inspections, strata search

- Borrowing Costs e.g. loan application fee, valuations, LMI

- Government Charges e.g. stamp duty etc

- Conveyancer fees

- Home and Content Insurance

- Additional life insurance, income protection fees & moving in costs

How To Use Equity To Buy An Investment Property

Equity is the difference between the market value of your property and the amount you still owe against it. For example, if your home is valued at $500,000 and you currently owe $300,000 on your home loan, your equity in that property would be $200,000. If you then access $100,000 of that equity you will increase your borrowings aginst that property to $400,000. Being only 80% of the total value of the property, you will not have to pay LMI.

You could indeed borrow an additional $50,000 to take your borrowing to $450,000 but please bear in mind this will increase your borrowing on the property to 90% of the total value so you will have to pay LMI.

Loan Structure Options

- Cross Collateralisation

Cross-collateralisation is when more than one property is used to secure a loan or multiple loans. For example, a person owns Property A and wants to purchase Property B without using any of their own funds. In this instance, the lender can use both properties as collateral for the new loan.

Risks of Cross collateralizing:

You may limit additional borrowing as your equity is reduced.

Both properties are at risk of being sold by the lender if you default on your loan.

You are tied to a single lender

Potentially higher fees.

Avoiding Cross Collateralisation:

By NOT Cross Collateralising you are protecting your home against any potential problems with the Investment property. So let’s look at how this would typically be structured …..

Example:

Borrower owns property A valued at $500,000 with an existing home loan of $300,000 and $200,00 equity. The wish to purchase an investment property valued $400,000.

To avoid cross collateralising, they could use their equity and set up a draw down facility for $100,000 with their existing lender and use $95,000 to cover the 20% deposit plus costs for the investment.

Then, they would set up a new loan with a NEW lender for the remaining 80%.

Buying An Investment Property Using SMSF

SMSFs are Self Managed Super Funds and they can be used to purchase an Investment Asset where the investor has insufficient financial resources to purchase a desired investment asset without borrowings. This is a viable but highly complex option and must be discussed with your Accountant or Financial Planner. It is worth noting that:

The minimum amount required to open and SMSF is $200,000 and the maximum LVR allowable for residential borrowing is 70- 80% and is much lower for commercial or rural properties.

There are many fees included in borrowing through SMSF also.

SMSF Example

Jodie has $250,000 in her SMSF

She wants her SMSF to purchase an Investment Property valued at

$500,000

The SMSF will need to borrow $350,000, to purchase the INV

property, and still leave some cash in her fund

Parental Guarantor

Even with no deposit and no SMSF, there ARE ways to get into the property market NOW…

If you don’t have a deposit & your parents own a property you can consider a parental guarantor structure.

This means your family member using their own home equity to provide additional security for a portion of YOUR loan amount. This also reduces your LVR so can save you money.

This allows for 105% of the purchase price to be borrowed (including stamp duty and fees) and means you don’t need to pay LMI and better yet, you don’t need a deposit.

In order to facilitate this, some lenders will accept a 2nd loan on your parents’ home with sufficient equity while other lenders will require that your parents are working. Alternatively, a lender might use your parents’ investment property if they have one.

If you go down this route, always aim to remove the guarantee as soon as you owe less than

80% of the property value.

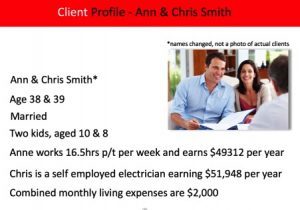

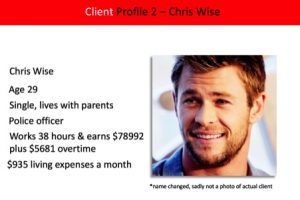

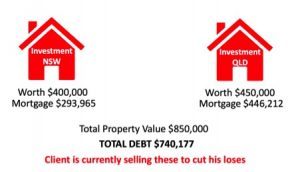

Do I Earn Enough To Invest In Property?

This is a question we hear often, and the answer differs with each scenario. So let’s look at a couple of real life examples of everyday investors …

Why Should You Use A Mortgage Broker?

A great mortgage broker will not only be skilled in finance but they will have access to many lenders and will understand their lending policies. They may also have access to rates that you would not have access to. A great broker will save you many hours, reduce your stress and ensure that your finance is structured correctly.

How Do You Find A Reliable Mortgage Broker?

Referrals – ask family, friends and colleagues

Testimonials – check websites & social media for reviews

Experienced? – Check experience on Linkedin

Qualified? – Check they have Diploma in Finance

Call – pick up the phone. Do you feel comfortable?

ABOUT LOUISA

Louisa Sanghera is principal Finance Broker and Financial Strategist at Zippy Finance and founder of Your Property Experts. Louisa has over 30 year’s experience in the Finance industry and is an expert in arranging finance for investment purposes.

About Author

Related posts:

{kind=link}